Written by: Wendy Rinella, CEO

With the official start of summer only a week away, it would be easy to assume that I am talking about a retail summer treat provider, but no, I am referring to the Disbursement Quota (DQ). This DQ is a federal government calculation of the minimum amount of its assets that a charitable foundation must distribute annually to qualified recipients and/or for charitable purposes as a share of its assets.

On April 7, 2022, Finance Minister Chrystia Freeland tabled the 2022 Federal Budget. One of the key proposals affecting charities in Budget 2022 is an increase in the DQ from a minimum of 3.5% to 5.0% by January 1, 2023. While there is another key change affecting funding relationships between charities and not-for-profits, I will focus on the DQ issue as I have heard a number of comments and requests for further information about this issue.

Here are some of the questions I have been asked:

1. Why is this an issue?

At its core, the growth in granting of charitable foundations has not kept pace with the growth in assets. The other perspective is that there is significant need across the charitable sector, particularly in equity deserving communities and that the DQ is too low at a minimum of 3.5%.

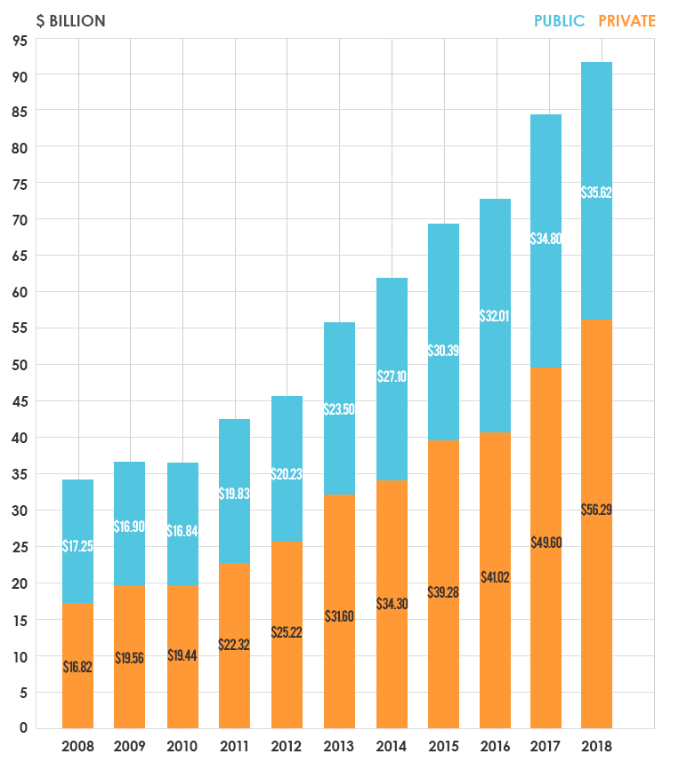

So let’s look at data that is publicly available about assets and granting of charitable foundations from Philanthropic Foundations of Canada. If you need a description of the differences between a public and private foundation, please see below.*

The chart (left) shows that in the decade between 2008 and 2018 the assets held by private foundations increased by 234% and the assets held by public foundations by 106%. At the same time, the growth in grants has not kept pace.

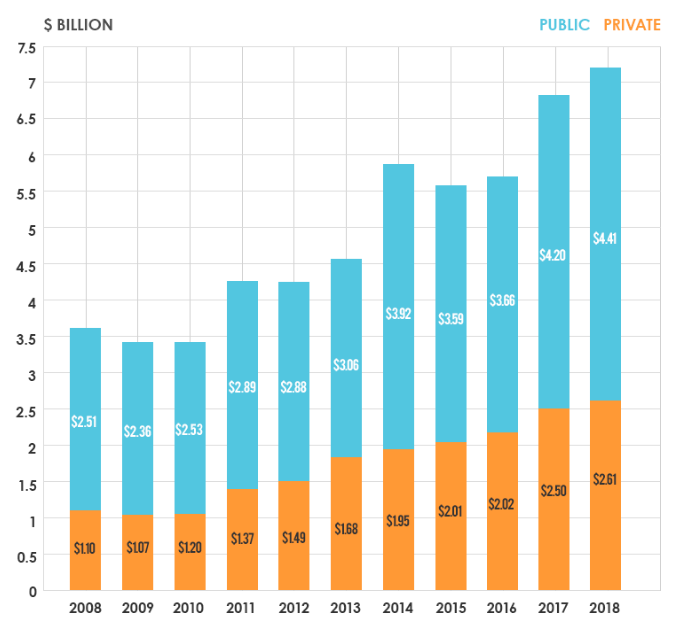

Public foundations make close to double the dollar amount of grants annually than private foundations (right).

While public foundations assets grew by 106%, their granting grew by 76%. While private foundations assets grew by 234%, their grants only grew by 137%.

So, traditionally, private foundations have granted at a lower rate and this difference has been exacerbated in recent years with the exponential growth of private foundations.

The Oakville Community Foundation is a public foundation. So, let’s look at our 2018 disbursements below.

Canadian public and private foundations held about $91.9 billion in assets and made $7.0 billion in grants in 2018. If we assess this one-year disbursement rate of grants to assets for public foundations it is 12.4%. Imagine Canada identifies that the majority of public foundations are not grant-making organizations like community foundations, but are attached to large institutions like hospitals, universities, etc, with large staff complements engaged in charitable work. If we assess the private foundation one-year disbursement rate, it’s almost one-third of the public foundation rate at 4.61%.

2. What is the Oakville Community Foundation’s DQ?

Since 2018, the Oakville Community Foundation’s DQ averages 7.4% as a result of grants and our own charitable activities (Community Classroom, Community Education Awards Hub, GIVEOakville, etc). For 2021, total grants were 6.09% and total charitable expenditure was 7.5% of our charitable assets. This distribution is double the current requirement of 3.5% and in excess of even the proposed increased DQ of 5%. Note: Assets that are held on behalf of other agencies and identified as liabilities on our balance sheet are not included in this calculation. They are included in that agency’s DQ.

3. Is the Spending Policy — the rate that Fundholders can grant every year — set at 3.5%?

It’s set through The Foundation’s Spending Policy at a MINIMUM of 3.5%. If a Fund has a positive balance in its retained income line item, a Fundholder can choose to advise on the distribution of those positive reserves for additional granting. For instance, in 2020 with the advent of the pandemic and, subsequently, when The Foundation launched the Resiliency Fund, many Fundholders advised on the distribution of their positive reserves to provide additional grants into the community.

4. Will The Foundation’s Spending Policy change and my available-to-spend increase?

Right now we are in compliance with the new requirements of a minimum 5.0% DQ. However, we do not know if there will be new criteria in the calculation of the DQ as the federal budget contemplates the possible removal of the ability of the charities to include allocation of administration and management fees in their DQ calculation.

The United States has a DQ of 5% as well, but all charity expenditures are included in their DQ calculation. There is no dividing up of charity expenses between charitable and administration activities, like in Canada. This is likely why administration spending by large American charities has come under scrutiny by donors when charities are housed in opulent offices, leasing luxury cars and golden busts of charity founders are acceptable expenses (a topic for another time).

In speaking with federal officials, the rationale for this change is that there is a concern that private foundations, who often employ their family members or wealthy family-office professionals like accountants, lawyers and investment advisors, will simply increase the salaries of these professionals to meet the new increased DQ.

While solving this issue in the private foundations, it creates a bigger challenge in public foundations like hospitals, universities or community foundations to redirect funds away from salaries to meet new DQ requirements. Like other public foundations, we have a publicly appointed Board of Directors and a foundation focused on supporting our local community. One of our main priorities for our new Strategic Plan is to pay all of our staff a living wage. Like other charities, we are struggling to ensure that we can provide a 5%+ inflationary increase to our majority-female staff salaries along with benefits.

So, removing the salaries and overhead from the calculation of the DQ may likely be a recipe for not increasing salaries for employees in public foundations. The sector is predominantly female and, in many cases, low income and racialized. This change will keep salaries at minimum wage, below a living wage, and feed even greater staff retention challenges for the sector.

I believe that the Federal government needs to adopt policies for private foundations that are separate from public foundations as they are two distinct creatures, with very different staff complements and should be treated thus, otherwise the impact will be contrary to the government’s commitments to women workers.

I have discussed this issue with local MPs, national advocacy groups like Imagine Canada, and Department of Finance Canada. The Department of Finance Director confirmed that he would share these concerns in his discussions of the guidance with the Canada Revenue Agency (CRA).

As this change to the DQ must be implemented by January 1, 2023, it requires The Foundation to consider making changes to both our spending policy and target investment return by the end of this year. Hopefully the CRA will provide guidance before then.

5. Why not just spend everything now if there is a need in the community?

Community Foundations are established with a mission to serve their local community and provide grants to local charities. They are established for the long term which is why most gifts to community foundations are endowed— which means the capital is held and invested in perpetuity. Long term capital creates stability for the community, the local charities, Fundholders’ granting and the community foundation operations.

While investment returns will fluctuate over time and thereby granting will fluctuate, by having a significant amount of endowed capital, the community foundation provides Fundholders and the local charities that they support with the comfort of stable funding to provide multi-year support from a one-time investment.

*A private foundation is usually established by a single individual, family or corporation and funded almost exclusively by the founders or close associates. While some private corporations have governance structures independent from their founders, the majority are closely managed and governed by the founders and their families.

A community foundation is a public foundation which derives its support from the public. It is governed by a diverse board of volunteers who are not related and elected by its members.